Brandon W. Mosley · UX Leader

Role UX Design Manager

Team Sr. UX Designer · Jr. UX Designer · UX Writer

Partners Head of Design & Research + UX Research · Product · Content Marketing · Engineering · QA

Deliverables User Stories · Design System · High-fidelity Prototype

Tools Figma · Sketch · Miro · Illustrator · Maze · User Testing

Timeframe 9 months

Company In-house

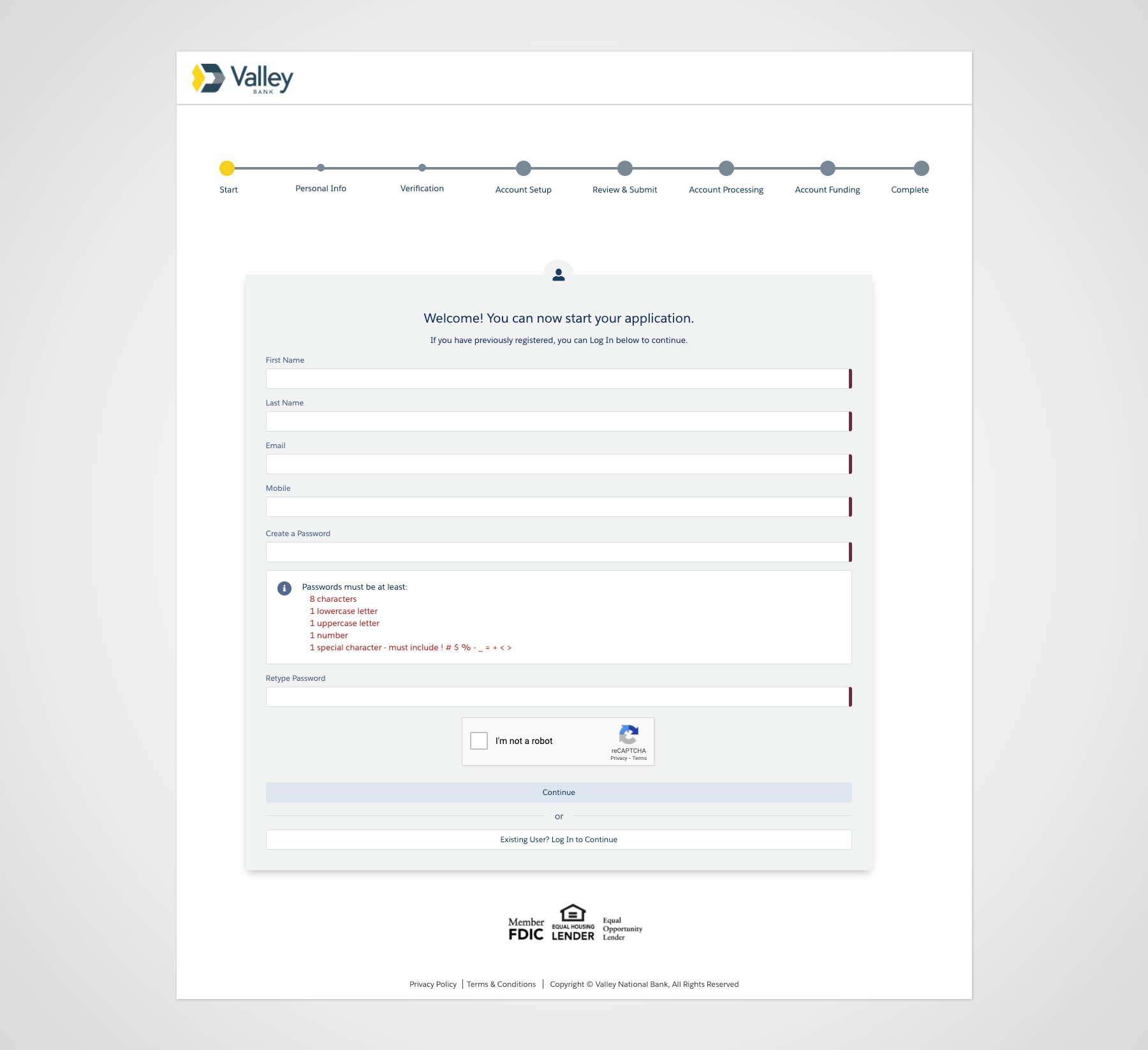

Banking with Valley was proven difficult during the pandemic when customers lost the white-glove service they experienced in branches. As part of its growth strategy to reach a wider audience, enable customers to expand their relationship with Valley, and offer products that meet customer goals, Valley initiated new digital account opening experiences using an off-the-shelf solution with limited customizations.

The current consumer account opening experience comprises over 12 arduous steps that take over half an hour to complete. The technology is old, and opening an account with Valley still requires manual paper and review processes, which slows the time to account opening.

Opening commercial deposit accounts is a time-consuming and tedious process compared to consumer accounts.

Learn more about how we solved account opening friction for new and existing customers >

"How do we enable customers to self-serve and expand our products and services nationwide while growing our assets?"

I initially partnered with UX Researchers and Product Managers to collect and synthesize analytical data and customer feedback that later informed design decisions. Today, I manage a team of designers and writers to continue the work.

As an off-the-shelf solution, the platform required a deep understanding of its component library.

Partnered with the UX Research Team and Experience Strategist to collect customer insights from listening programs and surveys, identifying opportunities to enhance the experience.

I generated user stories with scenarios and acceptance criteria, which helped the cross-functional team understand user tasks, define requirements, and generate QA testing scripts.

I lead weekly UX workshops with Product Managers, UX Researchers, Designers, and Writers, to define requirements and gather feedback on design concepts. These workshops involve some whiteboard and rapid prototyping.

An agency initially started the visual design process, which I took over and established a design system and improved the look and feel. I designed Over 70 new screens (including mobile designs) with a cleaner interface and created prototypes for user testing. My teamhas since evolved Valley's design system, which we rolled out across the account opening streams in Q2 2023.

I partnered with UX Researchers to test page flows for clarity, intuitiveness, and understanding of tasks. Testing mainly was successful, with some feedback suggesting clarity around language or labeling of instructions, buttons, and other UI components. I iterated on the designs based on user feedback. Today, I coach my direct reports to further design thinking practices. In some cases, I function as the UX Resesearcher and conduct usability testing within my unit.

Objective: Gauge how well users understand the process of adding beneficiaries to CDs.

Method: Unmoderated

Summary: Users find adding beneficiaries an intuitive and straightforward process with little friction, but it was not immediately apparent that the system added their beneficiaries to the CD. They prefer to actively save their designations or receive a confirmation that their input was successful.

Design Strategy

Objective: Gauge how well users understand why they cannot fund their accounts with a debit card after exceeding the $500 debit limit.

Method: Unmoderated

Summary: There's a high probability that users will reach the debit card limit, which prevents them from moving forward. Our mission was to determine how to best handle error reporting.

Design Strategy

Summary: User feedback and insights from exit-intent surveys and Hotjar session recordings revealed customer drop-off at the funding section. Evidence of pain points appeared when users encountered errors after skipping the funding area or attempting to link a bank account. We hypothesized that the language and required tasks weren't straightforward.

Design Strategy