Brandon W. Mosley · UX Leader

Role Director, Experience Design (UX Designer, Researcher, Writer)

Partners Product · Engineering

Deliverables High-fidelity · Content

Tools Figma · Maze · Miro

Timeframe 6-8 months

Company In-house

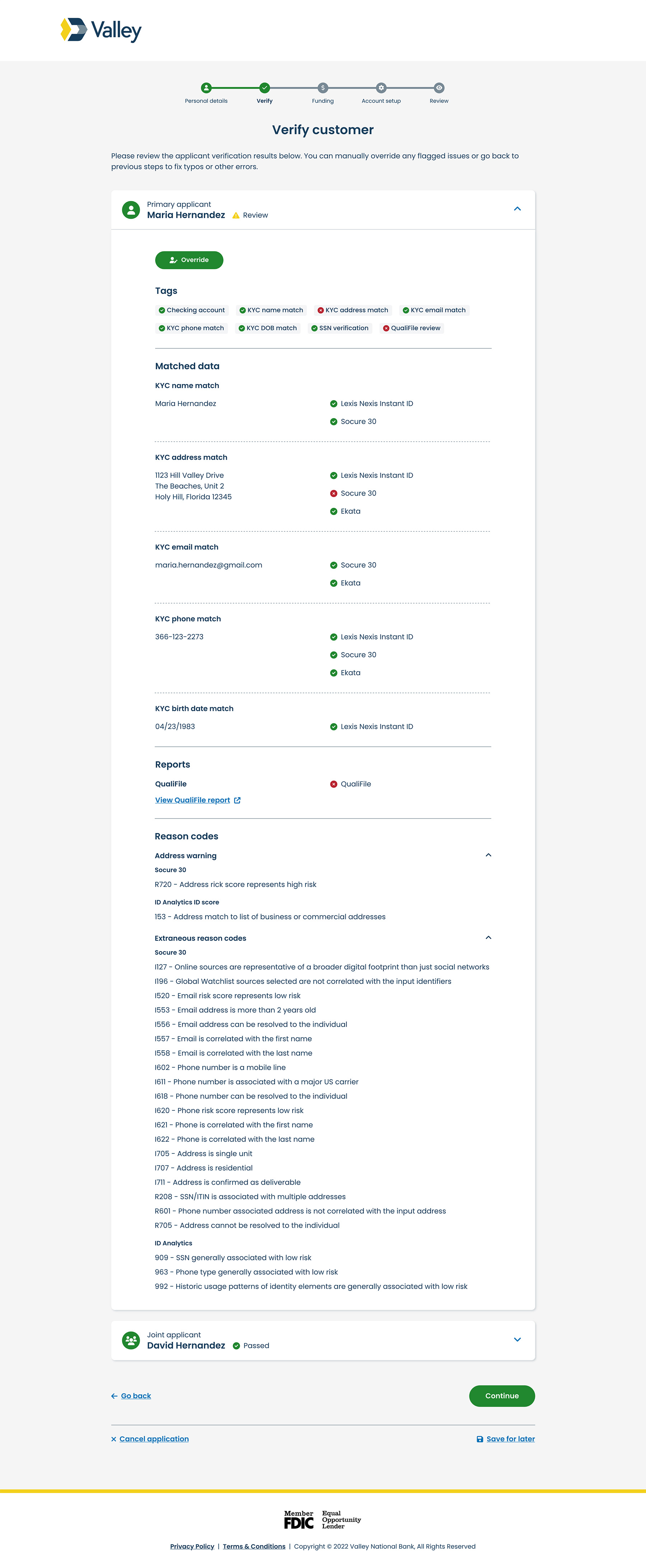

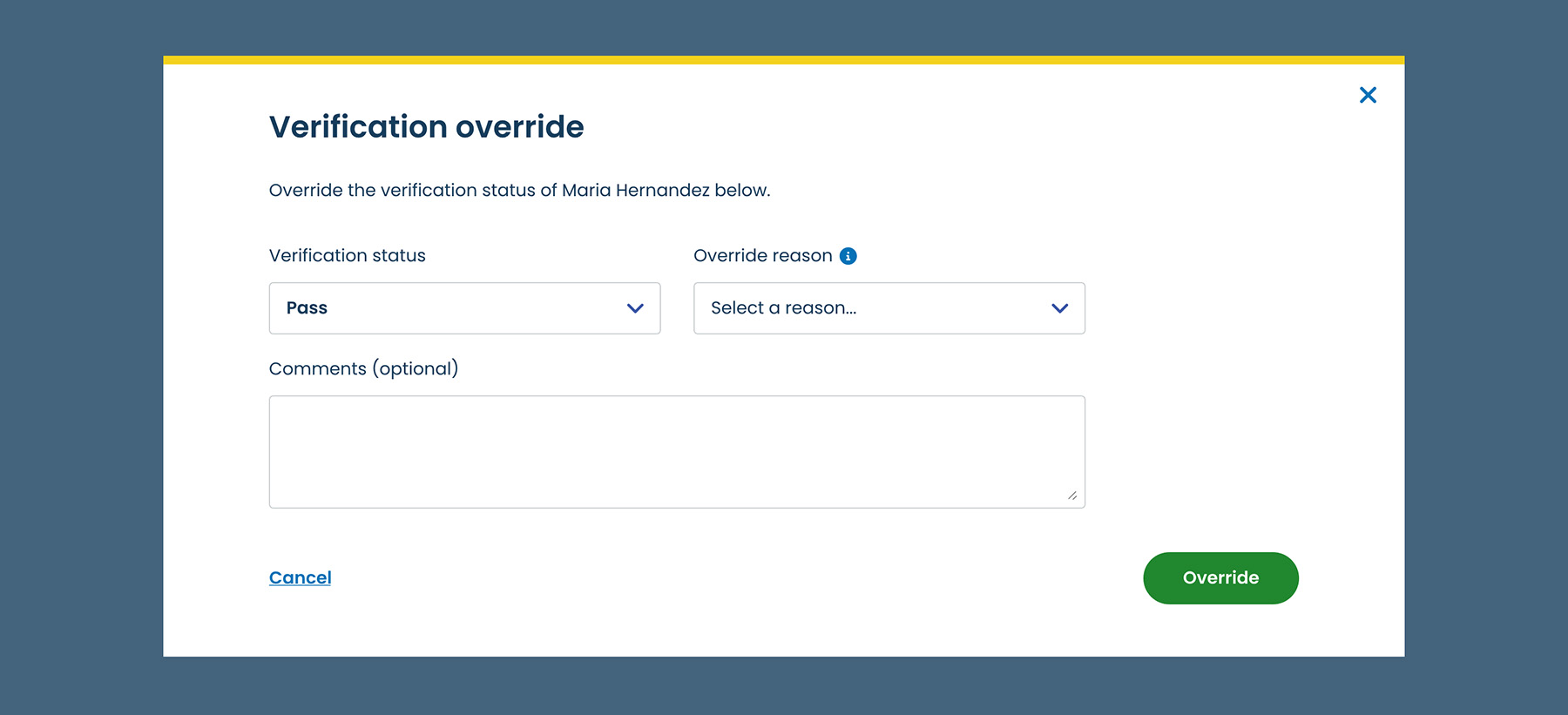

KYC (Know Your Customer) is a regulatory and operational framework used by financial institutions to verify the identity of clients during onboarding and throughout the customer lifecycle. It helps prevent fraud, money laundering, and identity theft.

The out-of-the-box solution presented screen comprehension and usability challenges, resulting in increased back-office corrections, onboarding delays, and compliance risks due to manual overrides and incomplete documentation. Over time, Experience Design and Product revisited the KYC flow as we learned about new user pain points.

Reimagine the KYC flow using moderated banker interviews and unmoderated usability testing to inform design and content decisions. The initiative aimed to:

While quantitative metrics were difficult to capture due to limited tracking of errors or call volumes, the team focused on:

Alloy (the fraud and compliance checks system) and Terafina (the account opening platform) heavily influenced the interface’s design due to their respective functionality. As UX Lead, I partnered with the UX Research team (a separate unit at the time) and Product to design an initial concept, which we tested with a pilot group of branch associates.

Overall, the research findings revealed a need for clearer on-screen guidance, more intuitive visual cues, and better support for edge cases.

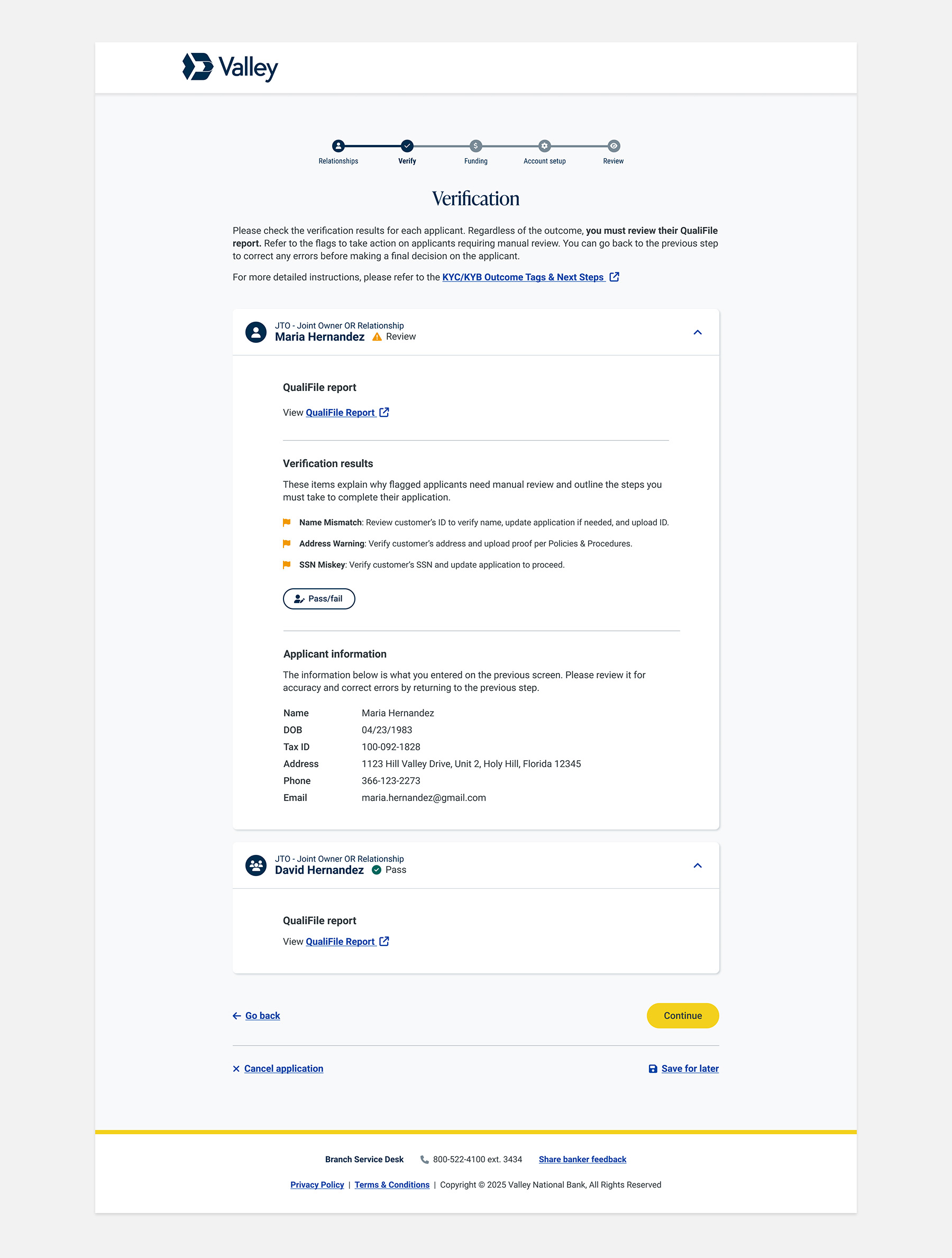

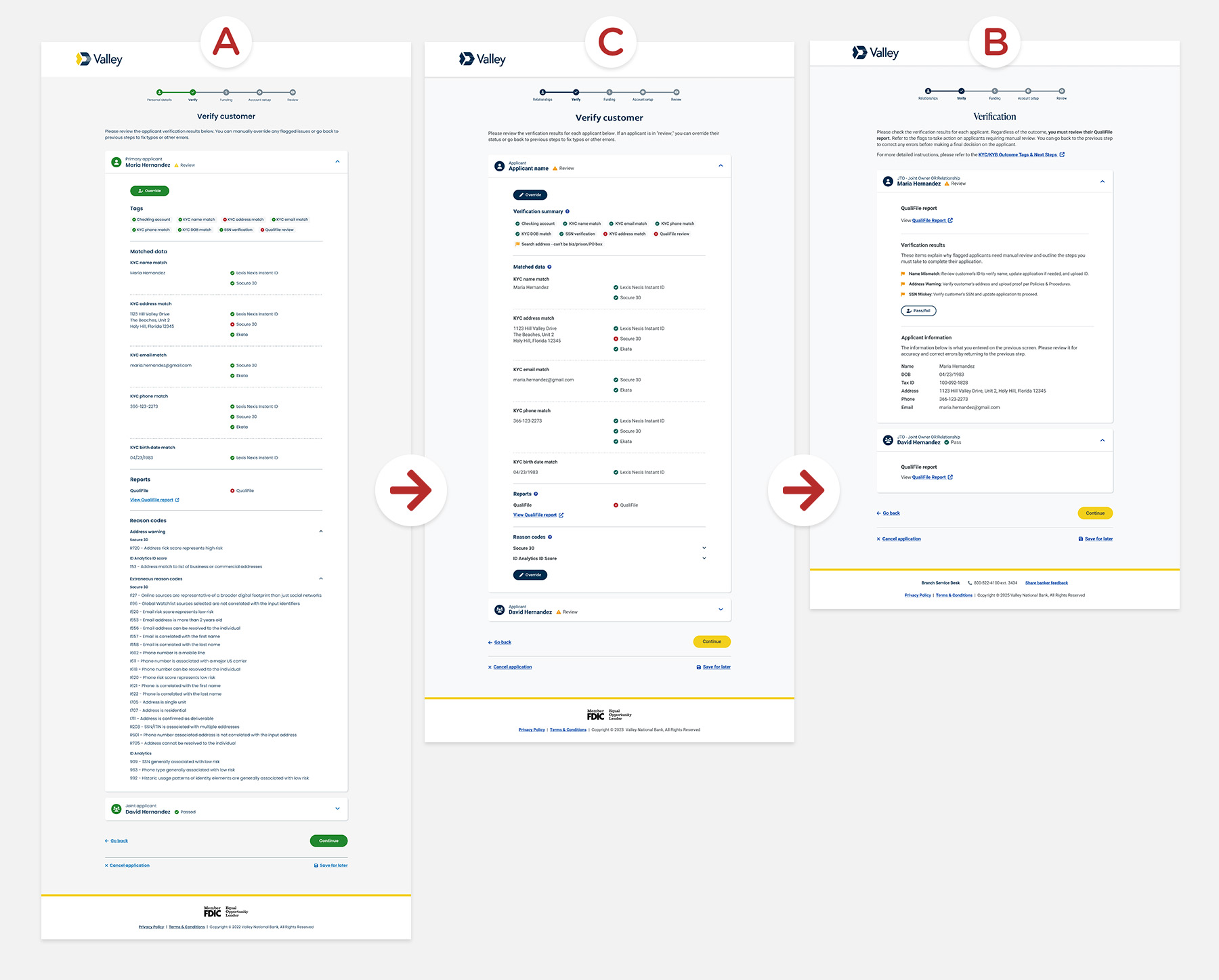

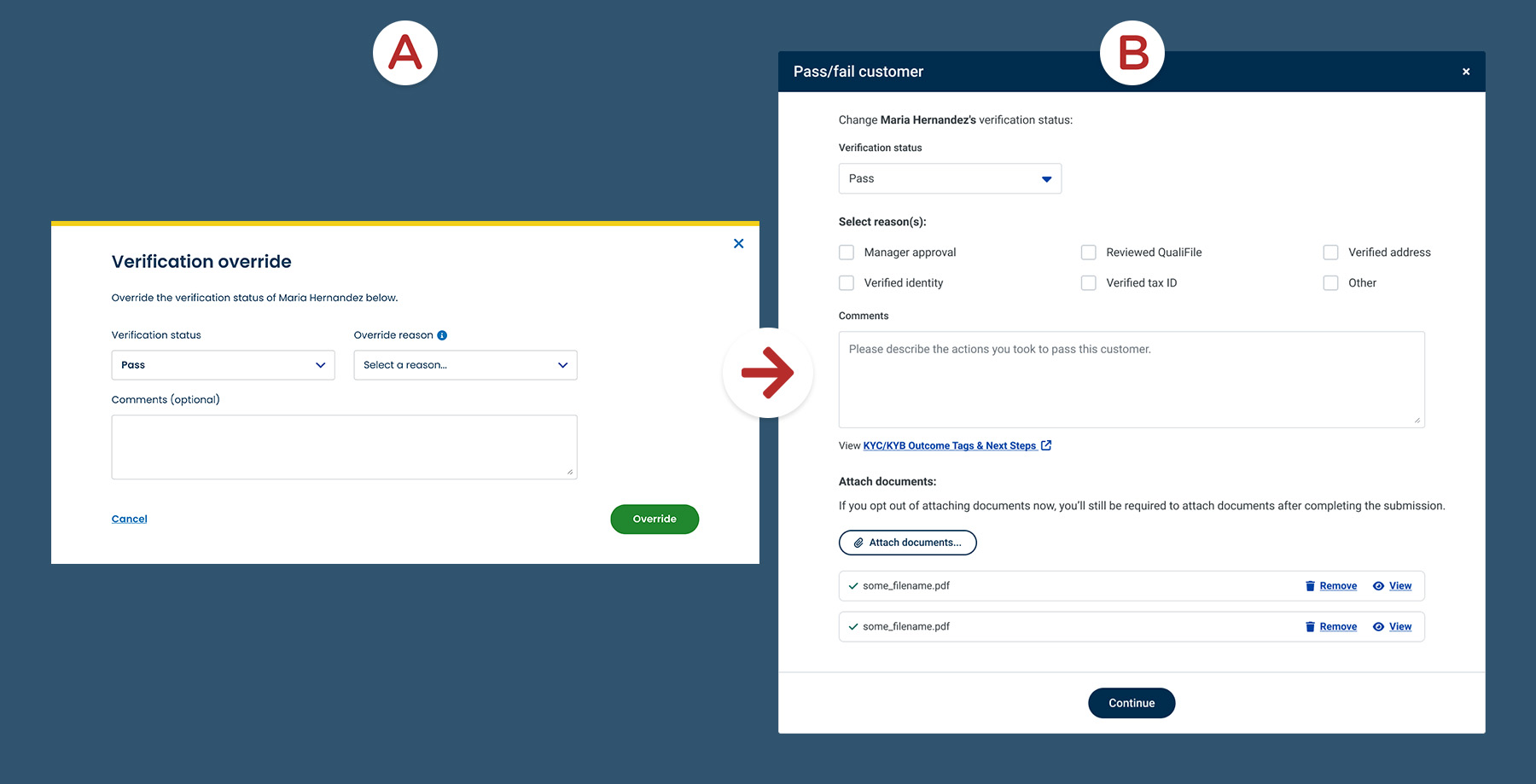

NOTE: By this iteration, we had rolled out the new design system.

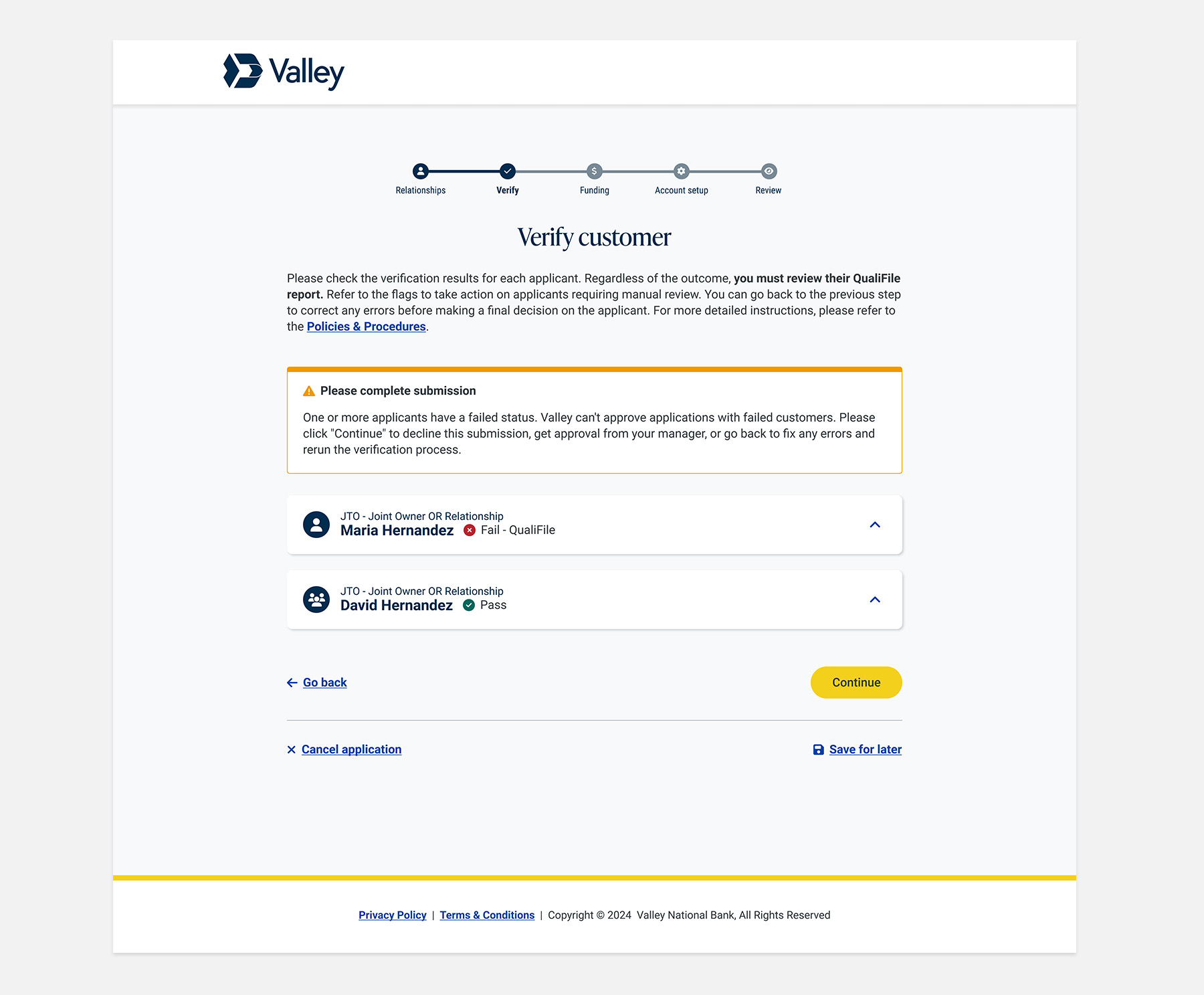

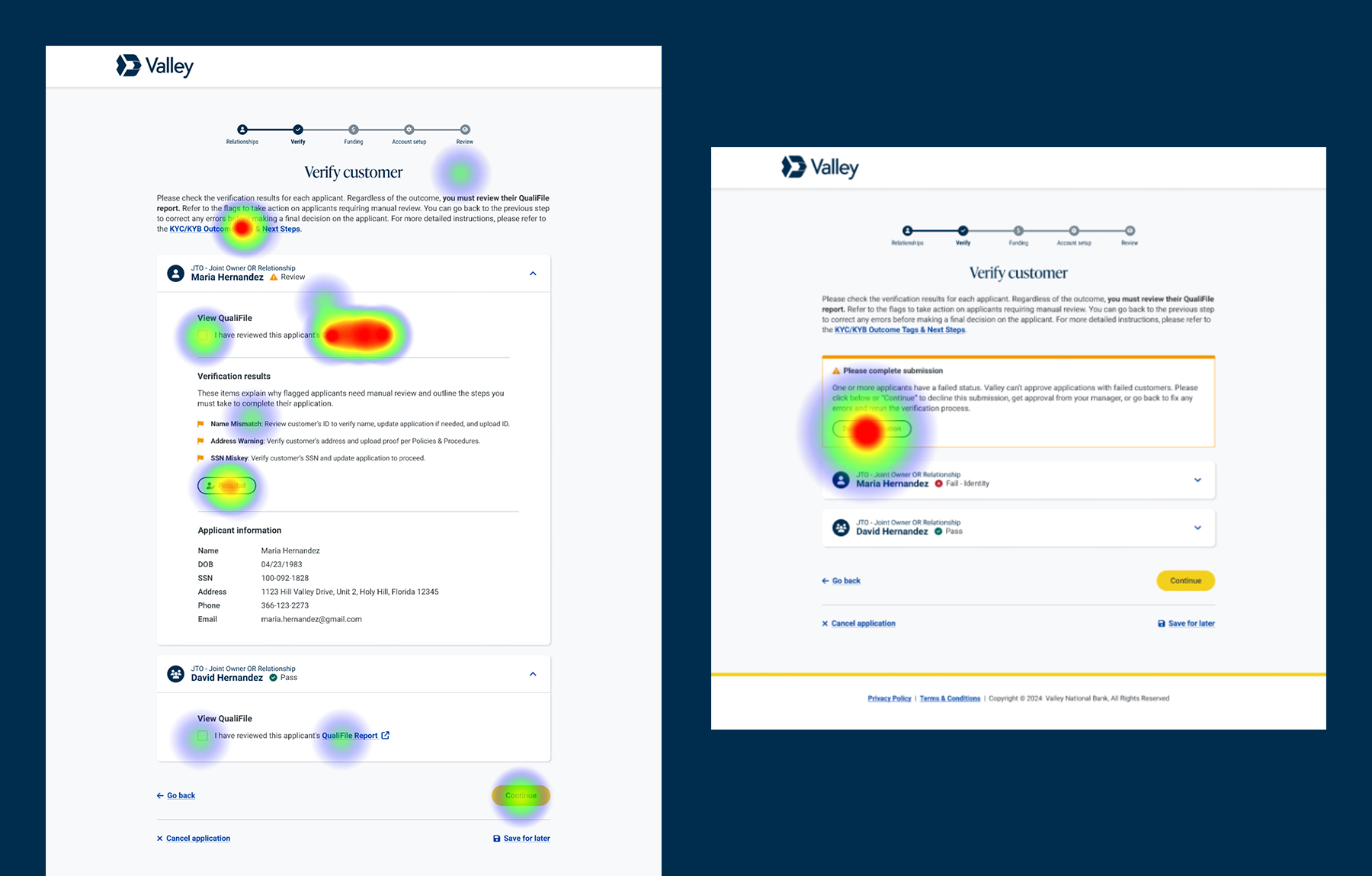

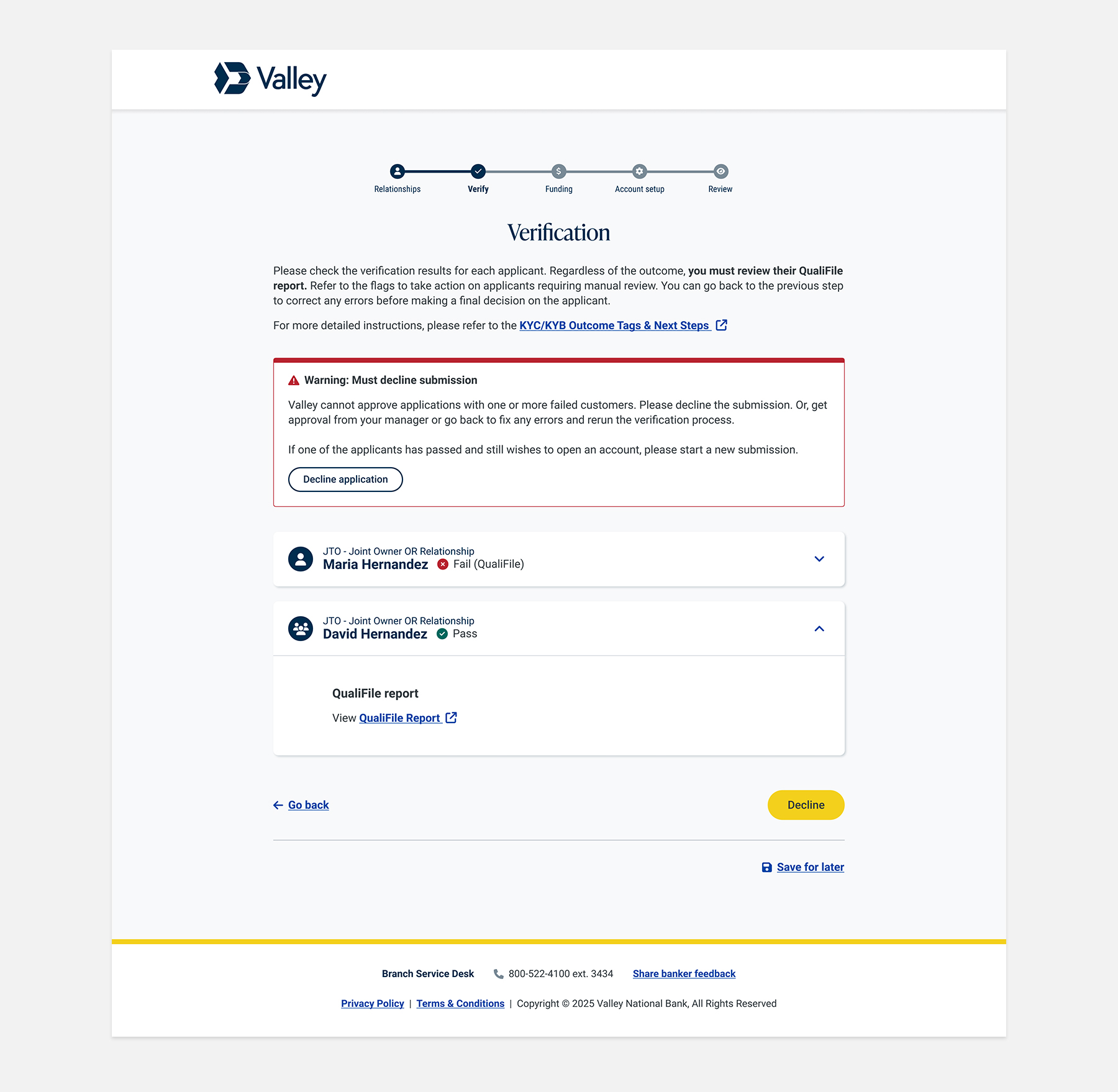

Since July 2024, 411 applications were returned with the QualiFile tag in a canceled, saved, abandoned, or expired state, among other errors. The Retail team provided direct feedback about persistent pain points and tasked us with addressing them by improving the interface. We learned that bankers mishandled applications requiring manual review, resulting in compliance issues and unhappy customers.

With a broader Experience Design team reporting to me by this time, I was still hands-on, but led UX Research and UX Design to improve and test a new solution.

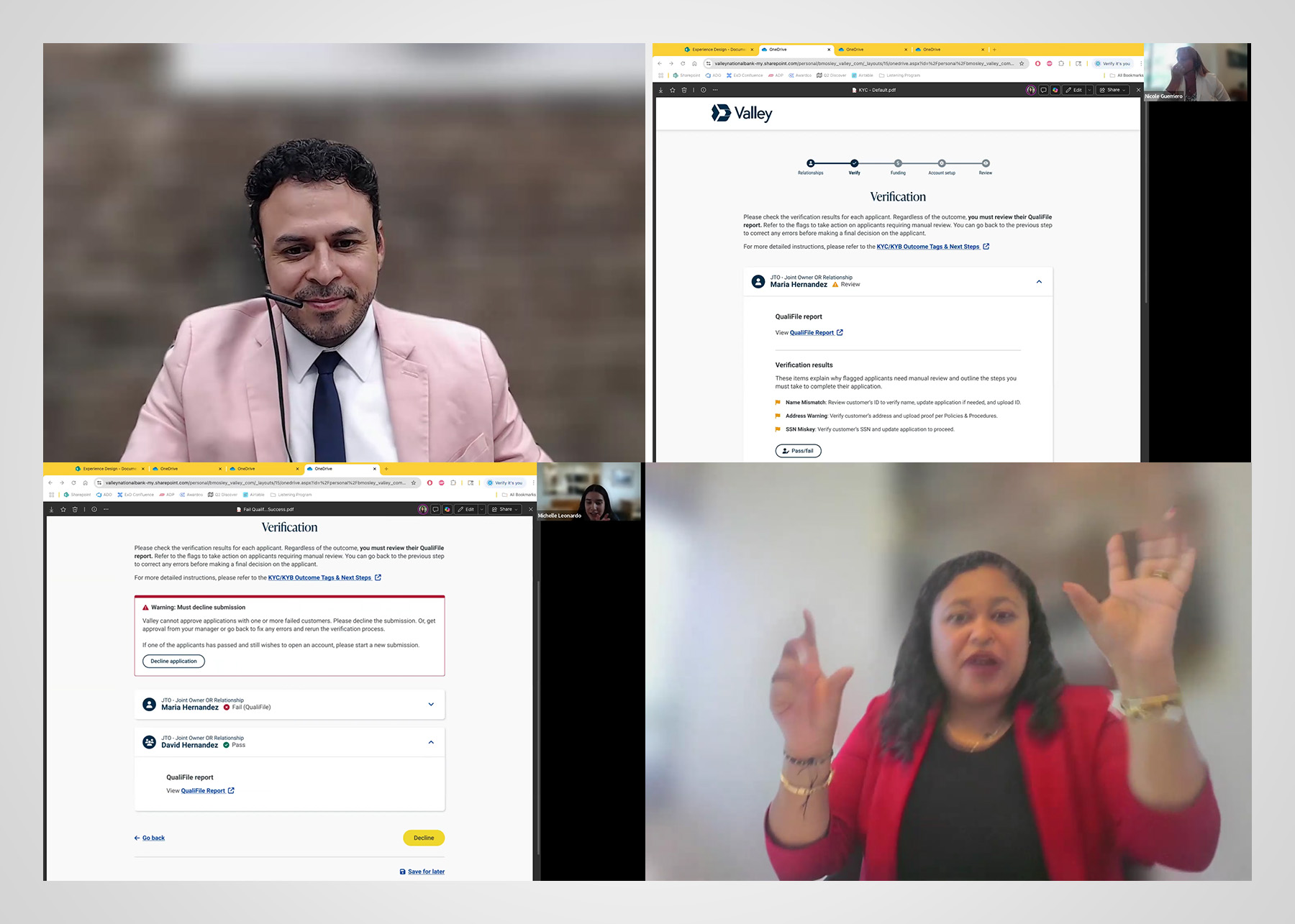

I led the UX research effort to conduct usability testing with branch employees who frequently appeared on the deficiency list. We also invited learning and development associates responsible for training bankers to participate.

“The QualiFile report helps to determine if we can open the account for the client or not, and to see the previous history of the client's banking.”

— Participant 338140112

“I would like the opportunity to select more than one reason (we may be asking a lot for personal bankers to select the most appropriate reason, or the branch manager might disagree).”

— Participant 334086386

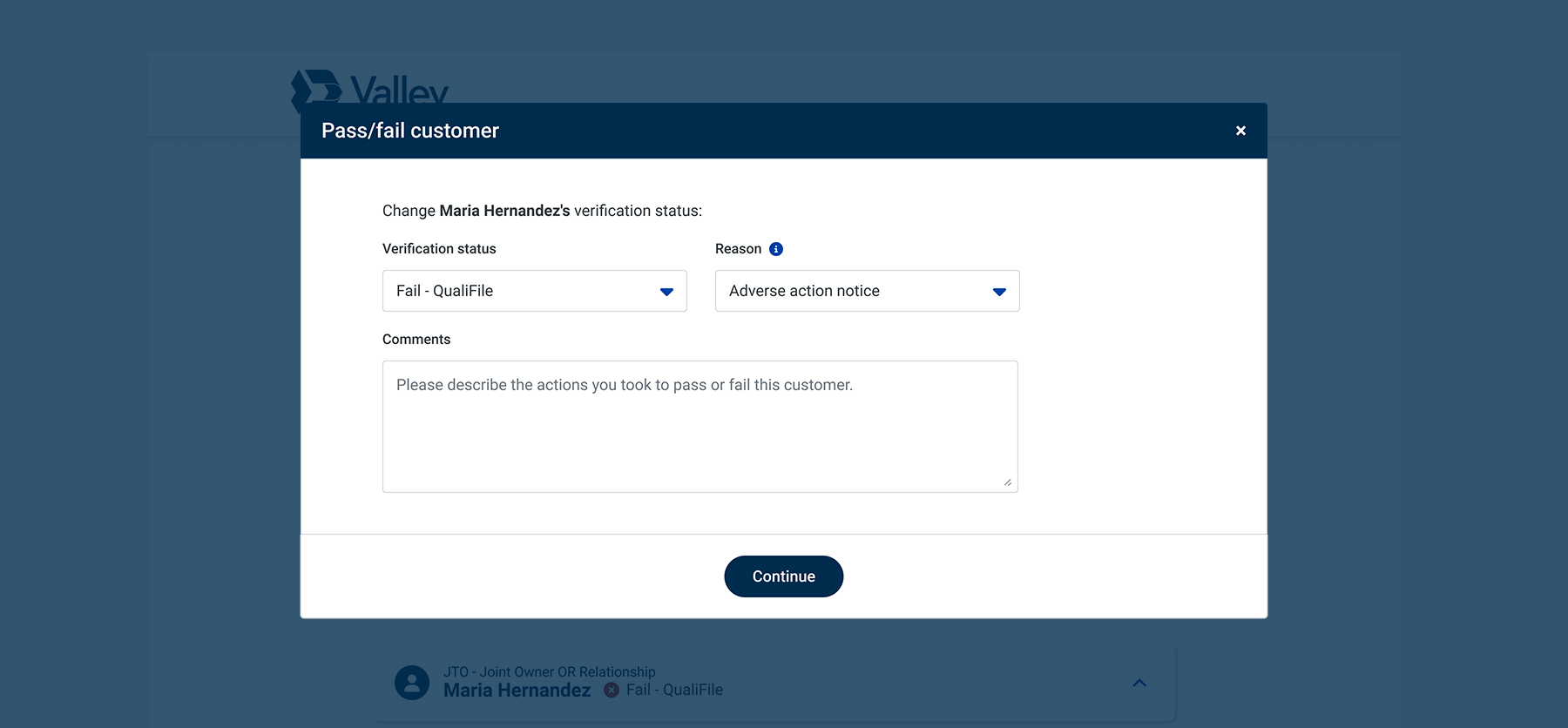

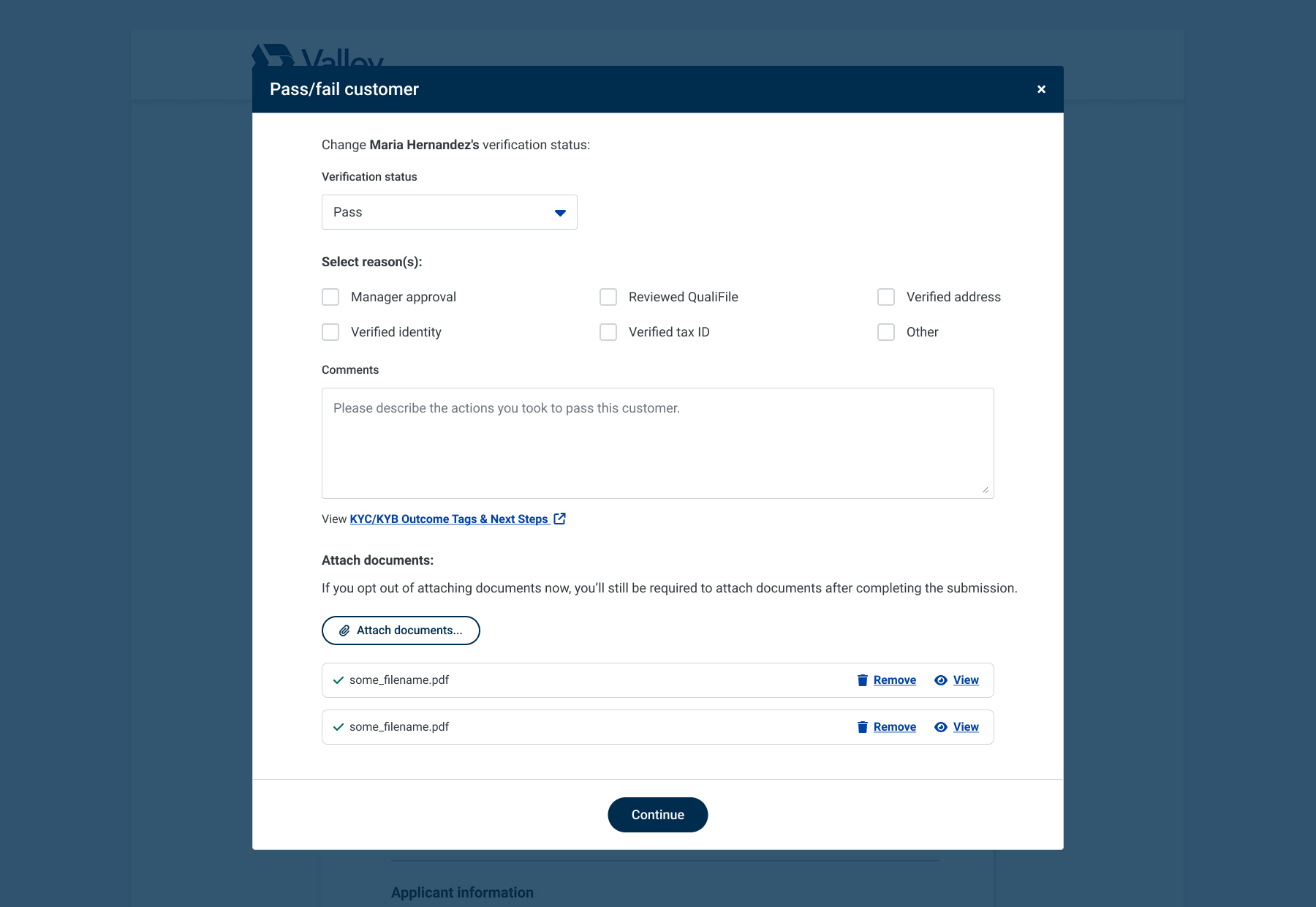

“The part where it said ‘click decline or click continue’ was a little confusing. I wasn't sure if clicking 'Continue' was just another way of declining, or if it meant I wanted an override from a supervisor.”

— Participant 337679316

“The flags seem clearer now, and I like that we can specify why the customer has failed.”

— Participant 337679316

“During the process, it would be great to be able to upload documents within the verification process, rather than after opening the account.”

— Participant 334628397

Overall, testers found the updated flow to be clearer and easier to understand, but there was still room for improvement to provide more step-by-step guidance, flexibility, and a clearer path to advance the application.

While we made improvements based on feedback from Retail and our studies, the data showed that bankers were actually mishandling more applications than before! How could this be possible? The question then was: why?

Despite the interface receiving very positive reviews, there was nothing further for UX Design to address. Our hypothesis is that bankers need better or more consistent training and improved support materials to guide them through the process. We believe there are deeper challenges—such as incentives and operational motives—that contribute to why some bankers continue to open applications incorrectly.

We shared our findings with Retail and Learning & Development to help close those gaps.

After multiple rounds of designing, testing, and learning from both banker and customer feedback, we continually evolved the banker’s experience over time. These ongoing improvements not only impacted bankers’ daily workflows and confidence but also enhanced the in-branch experience for customers by making processes smoother and more transparent.

Results are pending; expected outcomes include improved efficiency, compliance, and associate satisfaction, pending final measurement.